Debits and credits are two of the most basic principles in accounting, but most people nevertheless find them pretty darn confusing! We’ll help clear things up so you can get back to the business of making – and responsibly managing – money.

In the most basic sense, debits and credits are used to record every monetary transaction. You cannot have a debit without a corresponding credit to balance it out. But knowing that and being able to effectively track your own transactions are two very different things. And while we obviously aren’t going to provide anything approaching a Masters-level course in accounting, we can give everyday consumers and conscientious small business owners the tools needed to effectively track and manage their finances. Let’s get to work.

Real Life Example: Tracking Household Spending

We’ll begin with something familiar, tracking everyday income and expenses. Let’s say you’re the head of a household of four, with the following payment obligations and take-home pay:

- $50,000 Mortgage ($1,500 monthly payment)

- $15,000 Car Loan ($450 monthly payment)

- $10,000 Saved in a Checking Account

- $1,000 in Food Purchases

- $8,333 Monthly Paycheck

In the table below you can see how an average person might track these cash inflows and outflows to their checking account.

| Date | Item | Transaction | Balance |

|---|---|---|---|

| May 1 | Beginning Balance | - | $10,000 |

| May 1 | Mortgage Payment | -$1,500 | $8,500 |

| May 12 | Car Loan Payment | -$450 | $8,050 |

| May 20 | Food | -$1,000 | $7,050 |

| May 31 | Monthly Paycheck | +$8,333 | $15,383 |

| May 31 | Ending Balance | $15,383 |

Of course, most families will have more expenses than that, but this example gives us the foundation needed to talk about debits and credits. First, however, we need to nail down some ground rules.

Accounting Ground Rules

- Debits Always Equal Credits: The first thing to know is that when you debit an account there should be a corresponding credit to another account to balance it out. Debits are always shown on the left side of credits. If you keep this principle in mind, you will already know more than most people and can avoid many mistakes as you track your transactions.

- Assets = Liabilities + Equity: Assets are anything of economic value that you own or control. Liabilities are debts that you owe. Equity is the amount of an asset you own after you deduct what you owe on the asset. The total value of assets must equal liabilities plus equity.

- Temporary Accounts Track Cash: Revenue (Income) and Expense accounts are temporary accounts used to help track cash inflows and outflows. These accounts start the period with a zero balance. At the end of the period, any balance remaining in the account will be transferred to another account. This transfer is referred to as closing the account.

- Normal Debit Or Credit Balance: Each type of account (asset, liability, equity, revenue, and expense) has either a normal debit or credit balance. Accounts with normal debit balances are increased with debits; accounts with normal credit balances are increased with credits. The table below illustrates this principle.

| Type of Account | Normal Balance | Increase With | Decrease With |

|---|---|---|---|

| Asset | Debit | Debit | Credit |

| Liability | Credit | Credit | Debit |

| Equity | Credit | Credit | Debit |

| Revenue | Debit | Debit | Credit |

| Expense | Credit | Credit | Debit |

Accounting Examples: Journal Entries & T-Accounts

Journal Entries:

Using the accounting ground rules, we can show how accountants would track the same transactions using journal entries based on debits and credits.

| Date | Account | Debit | Credit |

|---|---|---|---|

| May 1 | Mortgage Loan Checking Account |

1,500 | 1,500 |

| May 12 | Car Loan Checking Account |

450 | 450 |

| May 20 | Food Expense Checking Account |

1,000 | 1,000 |

| May 31 | Checking Account Income |

8,333 | 8,333 |

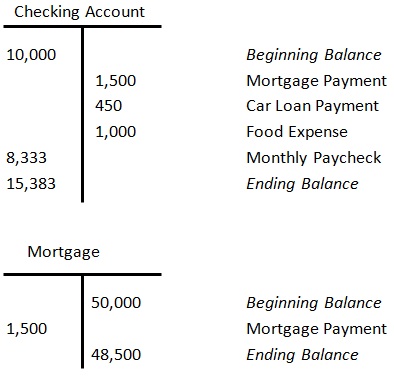

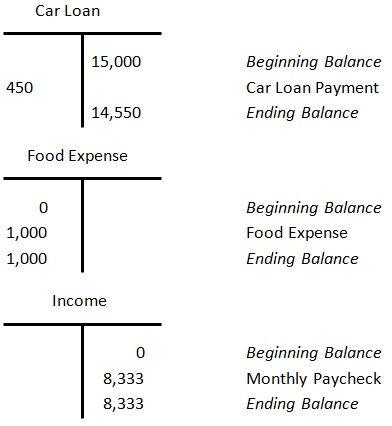

- Loan Payments: When you make loan payments you debit the loan accounts and credit the checking account, reducing the balance of each account.

- Food Expense: When you buy food, you debit an expense account and credit your checking account, reducing the balance of your checking account.

- Monthly Paycheck: When you receive your monthly paycheck, you debit your checking account and credit income, increasing the balance of your checking account.

T-Accounts:

A T-account is an accounting convention with which users can track debits and credits, placing debits on the left and credits on the right of a capital T’s base. T-accounts are used to show a journal entry’s effect on the different accounts. You will always need at least two T-accounts, one to debit and one to credit. Below you can see what the T-accounts would look like for our household transactions example.

The Final Step: Closing Temporary Accounts

If an accountant were tracking your money over the course of a month, as illustrated above, he or she would record journal entries each time you spent or received money. At the end of the month, the accountant would transfer those journal entries into T-accounts to get a final balance for each account.

The accountant would then “close” the temporary accounts by transferring those balances to another temporary account, called the Income Summary account. Finally, Income Summary would be closed and transferred to Retained Earnings, an equity account that accumulates income from each accounting period. These closing transactions ensure that Assets = Liabilities + Equity at the end of the month.

The following table may help you make sense of all that, but it’s important to remember that this is not something the average person will or should engage in. It is complicated, tedious work that is typically only undertaken in the context of traditional accounting. With that being said, here is what those closing entries would look like:

| Date | Account | Debit | Credit |

|---|---|---|---|

| May 31 | Income Income Summary |

8,333 | 8,333 |

| May 31 | Income Summary Food Expense |

1,000 | 1,000 |

| May 31 | Income Summary Retained Earnings |

7,333 | 7,333 |

After these closing entries, the Income, Food Expense, and Income Summary accounts all have a zero balance. The $7,333 in Retained Earnings will now make Assets = Liabilities + Equity.

| Account | Checking Account | Mortgage Loan | Car Loan | Retained Earnings |

|---|---|---|---|---|

| Type | Asset | Liability | Liability | Equity |

| Change | +$5,383 | -$1,500 | -$450 | +$7,333 |

Assets ($5,383) = Liability (-$1,500 – $450) + Equity ($7,333)

Key Terms & Other Info About Debits & Credits

Personal, and even small business, accounting is like a maze filled with debits and credits. We’ve already given you something of a map to follow, but in order to fully wrap your head around the issue, you must first firmly grasp the inherent importance of perspective.

For example, what you consider to be a debit from your perspective – a credit card payment, let’s say – would be an obvious credit from the credit card company’s point of view. That’s why it’s so easy to get turned around when talking about credits and debits – not to mention why we recommend a compass for home budgeting.

Keep that in mind as you explore a few other interesting aspects of the credit and debit world below.

- The Golden Rule of Accounting: This rule governs accounting principal and computation. Assets must always equal the sum of liabilities and equity. In other words, you may have $300K in real estate assets if you have $250K in home equity and a $50K mortgage balance.

- GAAP: This is an acronym for General Accepted Accounting Principles and describes the most common accounting methods used by corporations.

- Double-Entry Bookkeeping / Two-Account Rule: One of the earliest recorded forms of accounting, double-entry bookkeeping has its roots in medieval Europe and holds that every debit entry must have a corresponding credit entry. Every action in accounting has a corresponding reaction, if you will. A credit is the yin to a debit’s yang, in other words.

- Error Detection: Debits and credits must, by definition, equal one another. If your figures don’t match up, you’ll know you made an error somewhere along the way.

Double-entry accounting’s error detection capabilities are not infallible, though. Your credits and debits may still match up if your entries are in the wrong file or if they are mislabeled.

- Traditional / British / Costing Approach: This strategy relies on three types of accounts: 1) Real; 2) Personal; and 3) Nominal. Real accounts contain the assets and liabilities of the owner, while Personal accounts denote amounts owed to the owner and Nominal accounts denote revenue and expenses.

- Accounting Equation Approach: Also known as the American approach, this accounting method relies upon the Golden Rule of Accounting and uses five types of accounts: 1) Assets, Liabilities, Income/Revenues, Expenses and Capital Gains/Losses.

- Bank Debits & Credits: When you deposit money in your checking account, sometimes the banker will say, “I’ll credit your account.” This means your balance has increased. Similarly, a debit will decrease your account. This is because your deposits are considered liabilities (money owed) by the bank. Increases in your account mean that the bank owes you more money. Decreases in your account means that the bank owes you less money.

Ask The Experts: Should You Be Your Own Accountant?

- To what extent do you think dyslexia impacts one’s ability to budget?

- When should someone do their own household accounting vs. hiring a professional?

- What should people look for when hiring an accountant?

- Do you recommend any personal accounting software, and why?

Ask the Experts

Assistant Professor of Law at the University of New Mexico School of Law

Read More

Associate Professor of Finance at Delaware State University, College of Business

Read More

Associate Professor of Finance at Delaware State University, College of Business

Read More

Visiting Assistant Professor of Accounting at Le Moyne College, Madden School of Business

Read More

Visiting Assistant Professor of Accounting at Le Moyne College, Madden School of Business

Read More

WalletHub's personal finance experts are frequently cited by leading media outlets. Contact our media team to arrange an interview.