- Best Travel Credit Cards of July 2026 Compared

- Methodology

- Sources

- Beginner’s Guide to Travel Credit Cards

- About the Author

- Best Travel Credit Cards FAQ

Best Travel Credit Cards of July 2026 Compared

| Credit Card | Category | Annual Fee | Rewards Rate |

| Capital One Venture Rewards Credit Card (see Rates & Fees) | Best Overall | $95 | 2 - 5 miles / $1 |

| Discover it® Miles | Best for No Annual Fee | $0 | 1.5 miles / $1 |

| Regions Prestige Visa® Signature Credit Card | Best for Road-Trip Rewards | $0 | 1 - 3 points / $1 |

| Choice Privileges® Select Mastercard® | Best for Hotel Rewards | $95 | 1 - 10 points / $1 |

| Credit One Bank® Wander® American Express® Card with Dining, Gas & Travel Rewards | Best for Travel & Dining | $95 | 1 - 10% Cash Back |

| JetBlue Plus Card | Best for Airline Rewards | $99 | 1 - 6 points / $1 |

| American Express Platinum Card® | Best for Luxury Perks | $895 | 1 - 5 points / $1 |

The right travel rewards card is a very powerful tool capable of saving you a lot of money. You just have to find the right card for your needs.

Methodology for Selecting the Best Travel Credit Cards

More specifically, we calculate net rewards to estimate earnings after annual fees, and cards with lowest two-year costs are selected. These calculations, combined with analysis of the types of travel rewards cards people search for most often, lead us to the best travel credit cards in the most popular usage categories. We do not consider bonus rewards rates or redemption bonuses that require the cardholder to use the credit card issuer’s travel booking portal. These portals often have relatively high prices and limit customers’ options.

Finally, we repeat this exercise on a regular basis, updating our picks whenever offers change enough to warrant it.

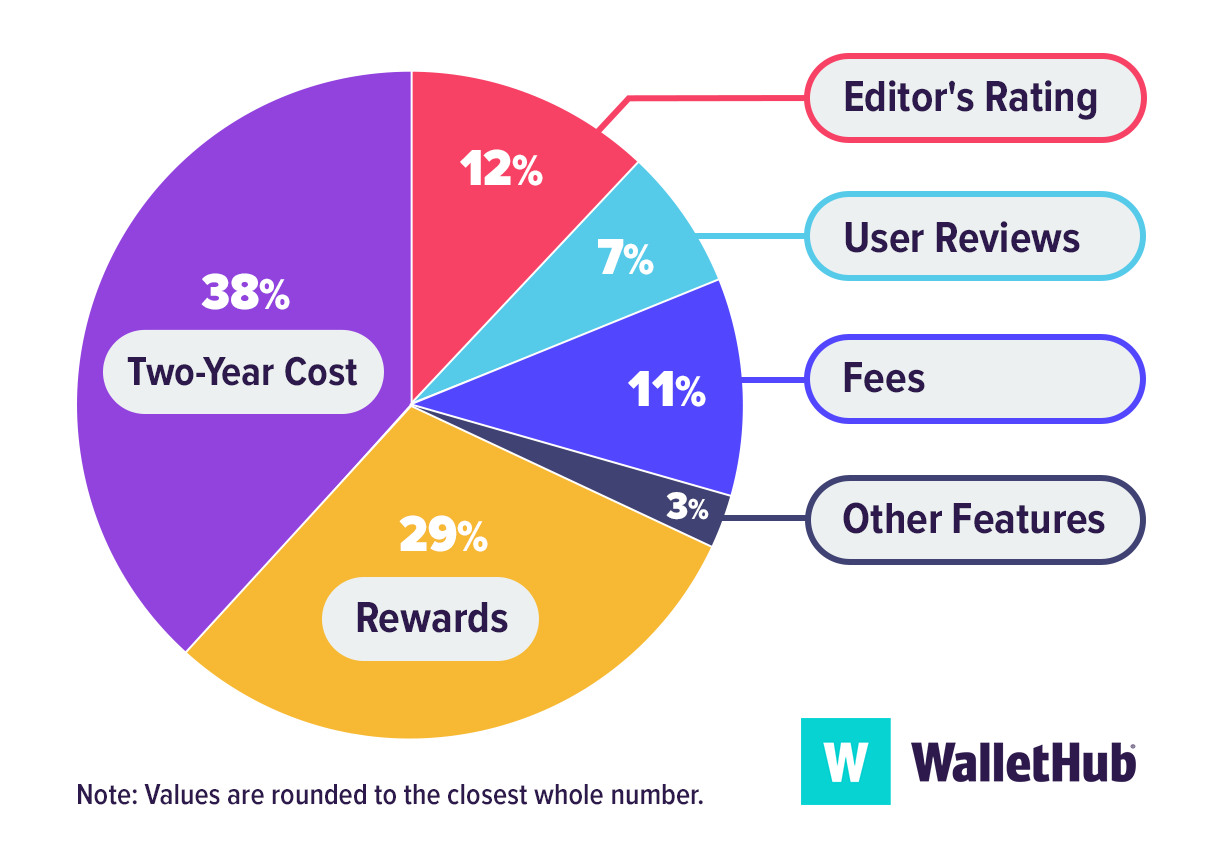

WalletHub’s Key Rating Components

Two-Year Cost: 38% - We calculate the estimated cost or savings over a two-year timeframe, factoring in fees, interest charges, and rewards. Negative figures indicate overall savings.

Two-Year Cost: 38% - We calculate the estimated cost or savings over a two-year timeframe, factoring in fees, interest charges, and rewards. Negative figures indicate overall savings.

Rewards: 29% - We examine each travel card’s rewards program, with a focus on earnings from travel-related purchases and bonus categories, to assess overall earning potential and value.

Editor’s Rating: 12% - WalletHub editors provide ratings based on a thorough evaluation of each card’s travel features, terms, and overall value relative to competing cards.

Fees: 11% - We review all fees associated with each travel credit card, including annual, foreign fee, one-time, and ongoing charges, to determine the total cost of owning and using the card.

User Reviews: 7% - We factor in reviews to highlight on-the-ground reporting from cardholders.

Other Features: 3% - We assess travel-oriented perks such as airport lounge access, concierge assistance, travel and purchase protections, exclusive events, and other benefits that can enhance users’ travel experiences.

In addition, a couple of picks are made to address different needs and may have slight variations in their score distribution as a result. These include cards chosen for individuals with below-average credit scores.

How Two-Year Cost Is Calculated

Two-year cost is used to calculate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that different users have different goals and are likely to use their credit cards differently, we identified spending profiles that are representative of different users’ financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data for consumers and PEX data for businesses.

Sources

WalletHub actively maintains a database of 1,500+ credit card offers, from which we select the best travel credit cards for different applicants as well as derive market-wide takeaways and trends. The underlying data is compiled from credit card company websites or provided directly by the credit card issuers. We also leverage data from the Bureau of Labor Statistics to develop cardholder profiles, used to estimate cards’ potential savings.

Beginner’s Guide to Travel Credit Cards

What Is a Travel Credit Card?

A travel credit card is a card that offers bonus rewards for travel-related expenses and allows you to redeem those rewards for things like free flights or hotel stays. Some elite travel cards also provide perks such as airport lounge access, travel insurance, and hundreds of dollars in travel credits.

Key Things to Know About Travel Credit Cards

- Travel credit cards can be co-branded with a particular airline or hotel chain, or they can be general travel credit cards that don’t limit your rewards to a specific company.

- You’ll typically earn more rewards with travel-related purchases compared to other purchases.

- The rewards you earn are usually worth the most when redeemed for travel.

- Travel credit cards normally offer rewards in points or miles.

- Most travel cards save you money abroad by not charging foreign transaction fees.

- Travel credit cards often let you transfer points or miles to partnered airline and hotel loyalty programs.

Learn more about travel credit cards.

How Travel Rewards Credit Cards Work

Travel credit cards work just like any other rewards credit card. You can use them to make purchases on credit, and you’ll earn points or miles on every dollar you spend. The rewards will usually appear in your account after the end of the billing period in which you earned them, though you may be able to get them sooner depending on the issuer of your card. Once you receive your rewards, you can typically redeem them for travel or a variety of other things like cash back, gift cards, or merchandise.

You’ll also have to make at least a minimum payment on your balance by the due date each month. If you don’t pay in full, you’ll generally spend a lot more on interest than you earn in rewards.

Differences From Other Credit Cards

The main thing that’s different about travel credit cards is that they tend to reward cardholders more for making travel-related purchases than anything else. Plus, the points or miles that travel credit cards provide are usually worth more when redeemed for travel, compared to other redemption methods.

There are different types of travel credit cards, too. Some give general rewards, while others are co-branded with various airlines, hotels or other travel providers and offer rewards in those companies’ loyalty programs.

It is also worth noting that travel credit cards commonly offer features such as travel insurance, no foreign transaction fee, airport lounge access, and reimbursement for TSA PreCheck/Global Entry application fees.

Learn more about how travel credit cards work.

Types of Travel Credit Cards

1. Airline Credit Cards

Credit cards affiliated with airlines help frequent flyers earn free flights and enjoy seat upgrades, priority boarding, free checked bags, in-flight savings and other perks. Most major airlines have affiliated credit cards, and most airline credit cards require good credit or better for approval.

Average Mile/Point Value by Airline

| Rewards Program | Average Value of 1 Mile/Point |

| American Airlines AAdvantage | 1.52 cents |

| Delta SkyMiles | 1.14 cents |

| Southwest Rapid Rewards | 1.21 cents |

| Frontier Miles | 0.98 cents |

| Alaska Atmos Rewards | 1.47 cents |

| Hawaiian Atmos Rewards | 1.71 cents |

| JetBlue TrueBlue | 1.37 cents |

| United MileagePlus | 1.21 cents |

| Virgin Atlantic Flying Club | 1.63 cents |

| Free Spirit | 1.07 cents |

| Sun Country Rewards | 1 cent |

Note: The table above includes major U.S. airlines that offer at least one credit card.

WalletHub calculated the average mile/point values by comparing flight rates between U.S. cities and popular travel destinations – both domestic and international – to the number of miles needed to book a flight. We applied the process to round-trip flights from Friday to Monday for each destination’s high and shoulder tourist seasons.

The values listed above are approximate and intended for illustrative purposes only. Actual mile/point values may vary based on redemption method and individual usage. The estimates provided do not represent fixed or guaranteed values and may differ from the experience of typical cardholders.

2. Hotel Credit Cards

Hotel credit cards have rewards tailored to specific hotel chains, which help frequent guests earn free nights and provide perks such as elite status, early check-in and late check-out. Major hotel chains from Hilton and Marriott to IHG and Hyatt have their own credit cards, and most require good credit or better for approval.

Average Point Value by Hotel

| Rewards Program | Average Value of 1 Point |

| Marriott Bonvoy | 0.79 cents |

| Wyndham Rewards | 1.09 cents |

| World of Hyatt | 2.38 cents |

| IHG One Rewards | 0.66 cents |

| Radisson Rewards | 0.61 cents |

| Drury Rewards | 0.86 cents |

| Hilton Honors | 0.55 cents |

| Best Western Rewards | 0.64 cents |

| Choice Privileges | 1.3 cents |

| Sonesta Travel Pass | 1.02 cents |

WalletHub calculated the average point values by comparing room rates in 20 popular travel destinations – 10 domestic and 10 international – to the number of points needed to book a rewards night. We did this for all brand-owned hotel locations within 50 miles of the city center in each destination, applying the process to weekend and weekday dates in each destination’s high and shoulder tourist seasons.

The values listed above are approximate and intended for illustrative purposes only. Actual point values may vary based on redemption method and individual usage. The estimates provided do not represent fixed or guaranteed values and may differ from the experience of typical cardholders.

3. General Travel Rewards Cards

General-purpose travel rewards cards aren’t affiliated with a particular travel provider. They allow you to earn rewards points or miles at a competitive rate on all travel purchases and then redeem them to pay for any flight, hotel reservation or other travel expense you want. The best travel rewards cards require good-to-excellent credit, but you can often find good offers for people with lower scores, too.

4. International Credit Cards

International credit cards have no foreign transaction fee, tend to be on the Visa or Mastercard network, and may have chip-and-PIN functionality. International credit cards usually have good travel rewards, too.

5. Other Credit Cards With Rewards

Any credit card with rewards can help you save on travel. For example, a cash back credit card still rewards you for travel purchases, and you can redeem what you earn for a statement credit to help offset the cost of travel accommodations. However, keep in mind that many cash back cards charge foreign transaction fees.

6. Other Credit Cards

Any major credit card can be a travel asset, even if it doesn’t offer rewards. Credit cards provide great currency conversion rates, for example, and often have perks such as travel insurance. Besides, simply having a credit card for emergencies can come in handy.

Pros & Cons of Travel Credit Cards

| Pros | Cons |

| Big initial bonuses | Limited redemption options or lower value for cash back |

| High ongoing rewards rates | Points and miles can expire or lose value over time |

| $0 foreign transaction fees | High interest rates |

| Benefits such as travel insurance and airport lounge access | Higher annual fees |

The biggest advantage of travel credit cards is the potential to save more money overall than you might be able to with a cash back credit card. Travel rewards cards tend to offer more valuable initial bonuses and higher ongoing rewards rates, but you have to redeem your rewards for travel to maximize your savings. Redemption restrictions are the biggest disadvantage of travel cards. Cash back rewards are much more flexible.

Learn more about why it’s good to get a travel credit card and what travel-card disadvantages to watch out for.

Should You Get a Travel Credit Card?

You should get a travel credit card if it will save you more money than cash back credit cards, cards with general-purpose rewards points, and cards that bring other features such as 0% introductory APRs to the table. That is most likely to be the case if you:

- Travel out of town multiple times per year

- Have a good or excellent credit score of 700+

- Plan to pay your new card’s bill in full monthly

As with any rewards card, you’ll also need to spend enough for the rewards and supplemental benefits to outweigh any annual fees. If that’s unlikely to be the case, you may want to consider a travel credit card with no annual fee instead.

It’s also important to point out that a travel rewards credit card could end up being just one of several credit cards in your wallet. The choice you’re making between travel rewards and cash back now doesn’t have to be one that you stick with forever. You could always apply for another card in six months to a year. In fact, WalletHub’s Island Approach recommends having different credit cards for different purposes.

Learn more about when getting a travel credit card is worthwhile.

How to Choose a Travel Credit Card

Picking the best travel credit card may seem difficult at first, but once you know what to look for, it gets a lot easier. Here’s what you need to do:

- Narrow down the options to cards you can qualify for, based on your credit score. You can check your latest credit score for free here on WalletHub, with daily updates.

- Get pre-approved for some of the cards you’re interested in, if their issuers let you check. This helps you gauge your approval odds before you apply, without hurting your credit score.

- Compare the expected net value (rewards minus fees) of your remaining choices. Don’t forget to factor in how an initial bonus might cover the fee for a year or more.

- Consider supplemental benefits. Many travel cards offer hundreds of dollars per year in extra value, but you have to actively take advantage of these benefits.

- Decide how long you want to use the card and where you want to use it, in order to finalize your choice and pick the best card for your needs. For example, if you plan to need a travel card long-term, don’t focus as much on the initial bonus – make sure the card’s ongoing rewards structure fits your spending habits. And if you usually use the same airline or hotel, consider one of their co-branded cards to maximize your rewards.

How to Make the Most of Your Travel Credit Card

Earn the Initial Bonus

Lots of travel credit cards offer lucrative initial bonuses for spending a few hundred to a few thousand dollars during the first few months the card is open. With most cards, it should be pretty easy to meet the spending threshold just by charging your essential monthly purchases to the card.

Maximize Your Rewards

Make sure to use your travel credit card for all of your travel purchases, as well as any other purchases for which the card offers a good amount of bonus rewards. This way, you’ll earn as many points or miles as possible.

Then, when you redeem, make sure to go for the redemption option that offers the highest value per point/mile. That will usually mean redeeming for travel rather than other options like cash back or gift cards.

Transfer Your Rewards If You Can Get a Better Value

Many travel credit cards allow you to transfer your rewards to the loyalty programs of partnered airlines and hotels (or sometimes even other types of travel providers like cruise lines). Depending on the program and the transfer ratio, you may be able to get more value for your points or miles by converting them to another program’s currency.

Take Advantage of Supplemental Benefits

Travel credit cards often provide travel insurance and rental car insurance for free, which can reimburse you if things don’t go as planned while you’re traveling. For example, you can get reimbursed for travel accidents, lost or delayed luggage, canceled or delayed trips, rental car accidents and more, depending on the card. All you have to do is file a claim.

Other common travel credit card benefits to look out for include:

- Yearly travel credits

- Credits for specific types of purchases (like the application fee for TSA PreCheck/Global Entry)

- Increased status levels in hotel/airline loyalty programs

- Special perks at certain hotel collections

- Free nights when you book a certain number of nights at a hotel

- Airline lounge access

- Free checked bags

- Priority boarding

- In-flight purchase discounts

Save Money on Purchases Processed Abroad

If you plan to travel abroad, make sure your travel credit card has a $0 foreign transaction fee (the vast majority of them do). This will save you up to 3% on purchases from foreign merchants. Having a card without a foreign transaction fee even saves you money when you’re just buying something online from a merchant based in another country.

You’ll also need to make sure you decline dynamic currency conversion when you travel abroad. This deceptive merchant practice offers to convert your purchase from the local currency to USD but charges conversion rates that can be more than 10% higher than normal.

Redeem Your Rewards Often

If you don’t redeem your points or miles regularly, it’s possible they could expire, depending on the terms of your rewards program. In addition, it’s possible that your issuer could devalue your rewards by making each point or mile worth less than it used to. While issuers aren’t really supposed to do this, it still happens.

Pay in Full Every Month

If you don’t pay your balance in full by the due date each month, you’ll start accruing interest on the remaining balance at the card’s regular APR. Doing that can quickly eat into any savings you might have gotten from rewards during the month. Paying in full ensures that you don’t owe any interest and your rewards are pure savings (after you’ve earned enough to offset any annual fee the card has).