- 5 Tips That Make It Easy to Get a Credit Card

- Easiest Credit Cards to Get in June 2026 Compared

- Methodology

- Sources

- About the author

- User questions & answers

5 Tips That Make It Easy to Get a Credit Card

You already have a major head start when it comes to finding an easy credit card to get. But we Hubsters are generous, so here are a few more pointers to ensure success.

1. Check Your Credit & Cash

You can’t know what you need without first assessing what you have. So check your credit score, review your free credit report and take stock of how much money you can attribute to monthly credit card payments. This will help narrow your options a lot as well as pay dividends in terms of account management.

2. Compare, Compare, Compare

Once you know what type of credit card you need, you should decide which terms are most important to you – no fee, rewards, 0% APR, etc. Then directly compare offers until you find the best deal.

3. Start with a Secured Card

The easiest credit cards to get are secured credit cards with no credit check such as the opensky® Plus Secured Visa® Credit Card because mistakes from the past or a limited credit history won't prevent you from being approved. The opensky Plus Card is an especially good choice because it has a $0 annual fee. It also reports monthly to the major credit bureaus, allowing you to build credit.

Getting a secured card will enable you to start the credit-building process as soon as possible. It will also give you complete control over your spending limit and help you avoid racking up debt, since your limit usually equals the amount of your security deposit. A secured card obviously won’t give you an emergency loan, though.

Unfortunately, decent unsecured credit cards for people with bad credit don’t really exist. They tend to charge high non-refundable fees and even higher interest rates in return for only a small amount of borrowing power. That’s why we always recommend biting the bullet and placing a deposit on a secured card.

4. Don't Forget Store Cards

Retailer-affiliated credit cards are surprisingly useful credit-improvement tools as they’re usually available to anyone with fair credit or better. Plus, very few of them charge annual fees and the best of the bunch offer some really great rewards.

5. Get Your Priorities Straight

When credit-improvement is your top priority, a low annual fee (or no annual fee) is the most important thing to look for in a credit card. Most credit-score damage involves missed payments, after all. So you should try to save as much money as possible, if only to build an emergency fund. Besides, if you have bad credit, you’re unlikely to qualify for good enough rewards or a low enough interest rate to warrant paying an annual fee when fee-free options are available.

Easiest Credit Cards to Get in June 2026 Compared

Some of the easiest credit cards to get are from banks that aren’t really household names. If you’d feel more comfortable with a card from a big bank, you can see a breakdown of the best options below.

| Card Name | Best For | Annual Fee | APR | Editor’s Rating |

| opensky® Plus Secured Visa® Credit Card | Easiest to Get | $0 | 28.24% (V) | 4.5/5 |

| Capital One Quicksilver Secured Cash Rewards Credit Card | After Bankruptcy | $0 | 28.99% (V) | 5/5 |

| Capital One Platinum Credit Card | No Credit | $0 | 28.99% (V) | 4/5 |

| Capital One Savor Student Cash Rewards Credit Card | Students | $0 | 18.49% - 28.49% (V) | 4.7/5 |

| First Progress Select Secured Mastercard® | No Bank Account | $39 | 17.49% (V) | 3.3/5 |

| OneMain BrightWay® Card | Unsecured | $0 - $89 | 35.99% | 3/5 |

| Amazon Secured Credit Card | Online Shopping | $0 | 10% | N/A |

Methodology for Selecting the Easiest Credit Cards

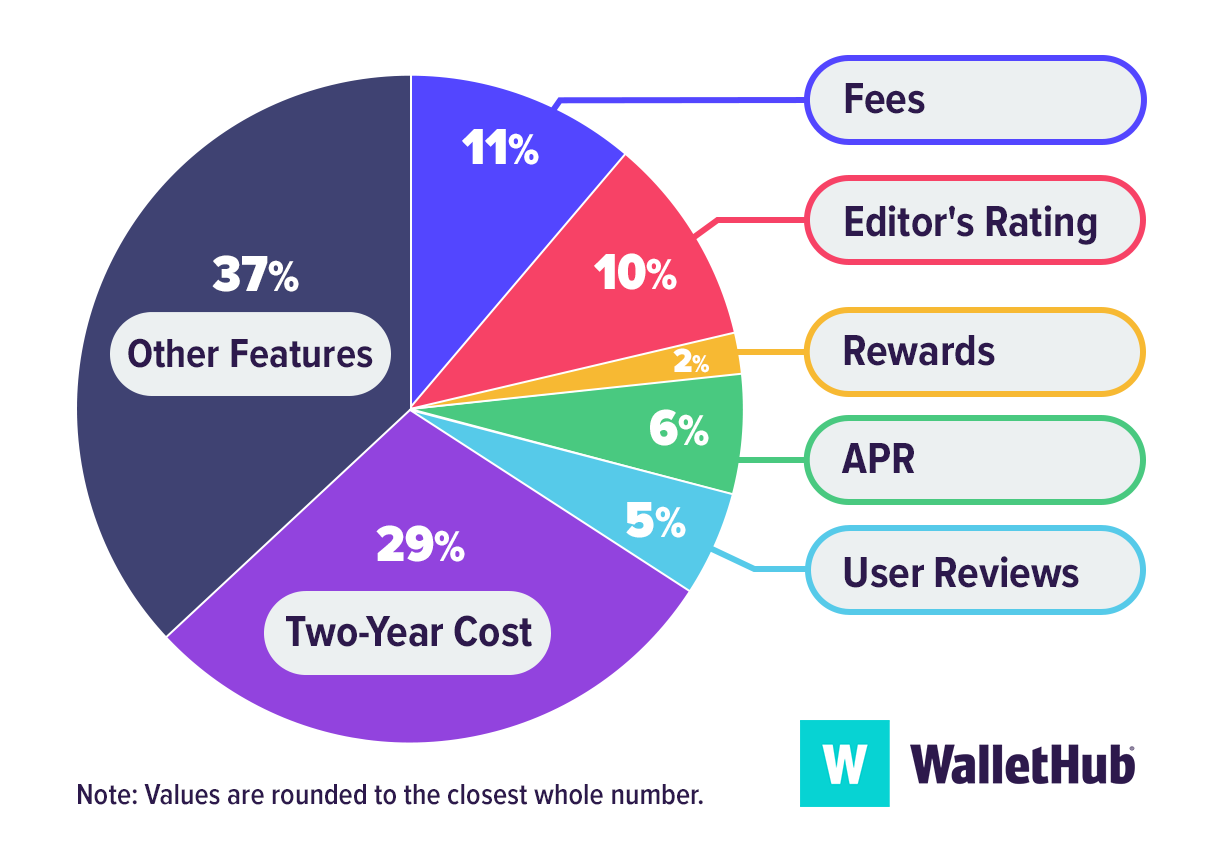

WalletHub's Key Rating Components

Other Features: 37% – We focus on features that make approval easier and more accessible, including easy-to-meet requirements, prequalification tools, instant approval decisions, reporting to all three major credit bureaus, refundable security deposits (for secured cards), and opportunities for credit limit increases.

Two-Year Cost: 29% – We estimate the total cost over the first two years for the average cardholder. This includes annual fees, monthly fees, required deposits, and any rewards earned.

Fees: 11% – We review all fees tied to the card, such as annual fees, monthly fees, and any upfront application or processing charges. Cards with simpler, more transparent fee structures score higher.

Editor’s Rating: 10% – Our editors evaluate each card based on ease of approval, affordability, credit-building potential, and overall value compared to similar cards.

APR: 6% – We estimate how much interest a typical cardholder might pay over two years based on the card’s ongoing APR and standard usage assumptions.

User Reviews: 5% – We include customer feedback to reflect experiences with the approval process, customer service, fee transparency, and day-to-day usability.

Rewards: 2% – We consider any rewards offered, giving preference to straightforward rewards that are easy to earn and redeem, though rewards are less important for cards focused primarily on easy approval.

A few cards use a slightly adjusted scoring methodology to reflect their unique purposes. They include student cards and store cards.

How Two-Year Cost Is CalculatedTwo-year cost is used to approximate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that people have differing goals and are likely to use their credit cards differently, we identified spending profiles that are representative of people’s varied financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data for consumers and PEX data for businesses.

Sources

WalletHub actively maintains a database of 1,500+ credit card offers, from which we select the easiest credit cards to get for different applicants as well as derive market-wide takeaways and trends. The underlying data is compiled from credit card company websites or provided directly by the credit card issuers. We also leverage data from the Bureau of Labor Statistics to develop cardholder profiles, used to estimate cards’ potential savings.