| Credit Card | Best For | Bankruptcy Eligible? |

| opensky® Plus Secured Visa® Credit Card | Overall | Yes (income must exceed expenses) |

| Capital One Quicksilver Secured Cash Rewards Credit Card | Rewards | Yes (discharged) |

| Credit One Bank® Platinum Visa® for Rebuilding Credit | Unsecured | Yes |

| Capital One Platinum Secured Credit Card | No Annual Fee | Yes (discharged) |

| First Progress Select Secured Mastercard® | Chapter 13 | Yes (discharged) |

Methodology

To identify the best credit cards to use after bankruptcy, WalletHub’s editors regularly compare more than 1,500 credit card offers based on their approval requirements, fees, minimum deposit amount, APR, rewards and other relevant WalletHub Rating components. In doing so, we focus on cards whose terms and conditions include language either explicitly stating that a recent bankruptcy does not make an applicant ineligible or that there is no minimum credit score or no credit check required.

WalletHub’s editors update these selections whenever new offers are introduced or existing offers change significantly.

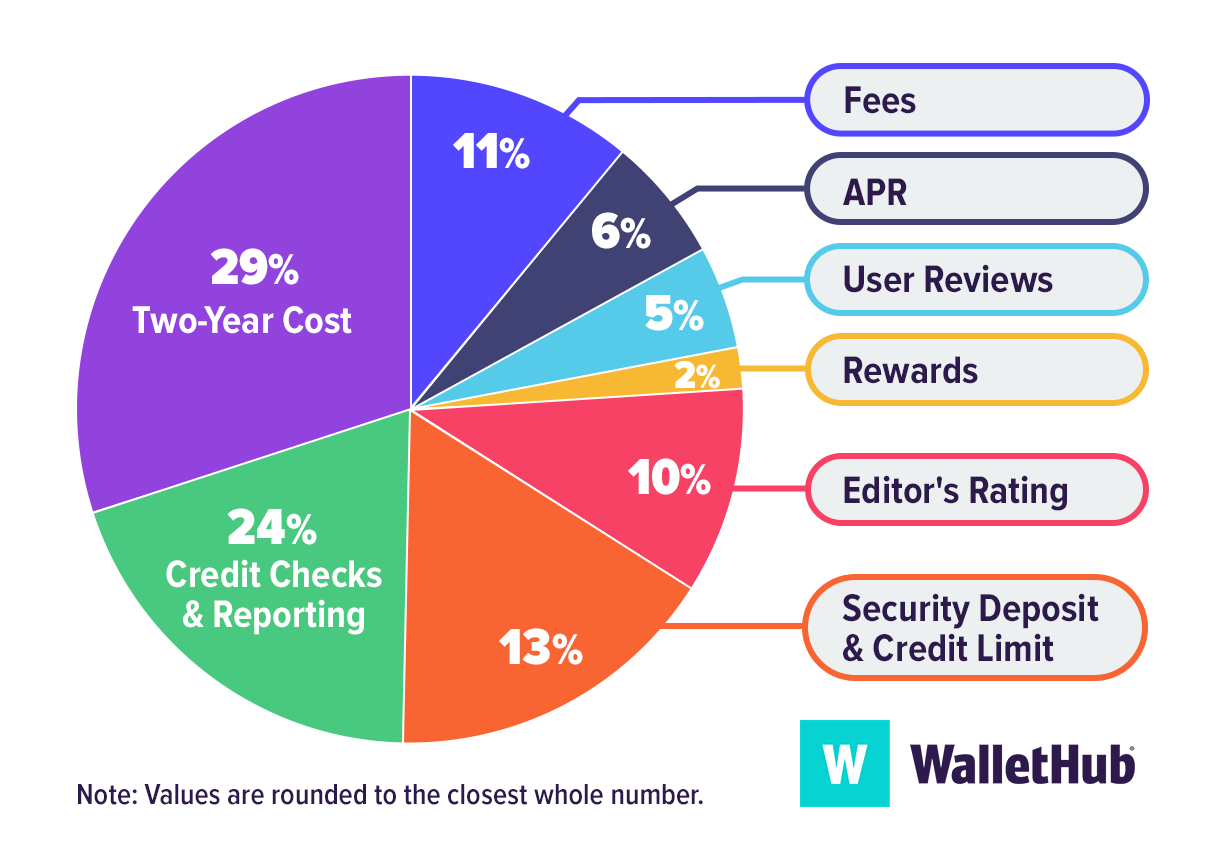

WalletHub's Key Rating Components

Two-Year Cost: 29% – We estimate the total cost over a two-year period, factoring in annual fees, monthly charges, security deposits (where applicable), and any potential rewards or statement credits.

Credit Checks and Reporting: 24% – We prioritize cards that are not only accessible to individuals rebuilding their credit after bankruptcy, but also conducive to long-term credit improvement. Our evaluation considers whether the issuer reviews your credit during the application process (and how strict the approval requirements are), whether approval is possible with a recent bankruptcy, and whether the card consistently reports payment activity to all three major credit bureaus. Reporting to the bureaus is essential for re-establishing positive credit history over time.

Security Deposit and Credit Limit: 13% – This category evaluates the upfront financial commitment required and the card’s flexibility as you recover financially. We review the minimum required security deposit (if applicable), how the deposit affects the starting credit limit, and whether there are opportunities for credit limit increases. We also consider whether the issuer offers a path to upgrade to an unsecured card or receive a deposit refund after demonstrating responsible use.

Fees: 11% – We carefully review all associated fees, including annual fees, monthly fees, processing fees, or any one-time setup charges.

Editor’s Rating: 10% – Our editors assess each card based on approval accessibility after bankruptcy, affordability, credit-building effectiveness, and overall value compared to other second-chance credit cards.

APR: 6% – We calculate the potential interest costs over two years using the card’s standard APR, based on typical usage assumptions for someone rebuilding credit.

User Reviews: 5% – We incorporate real cardholder feedback to reflect satisfaction with approval processes, fee transparency, customer support, and overall ease of rebuilding credit.

Rewards: 2% – While rewards are not the primary focus, we consider any cash back or points offered and evaluate how practical and attainable they are for cardholders.

Some cards featured here may prioritize rewards, and those options may be evaluated using slightly adjusted scoring criteria.