Methodology

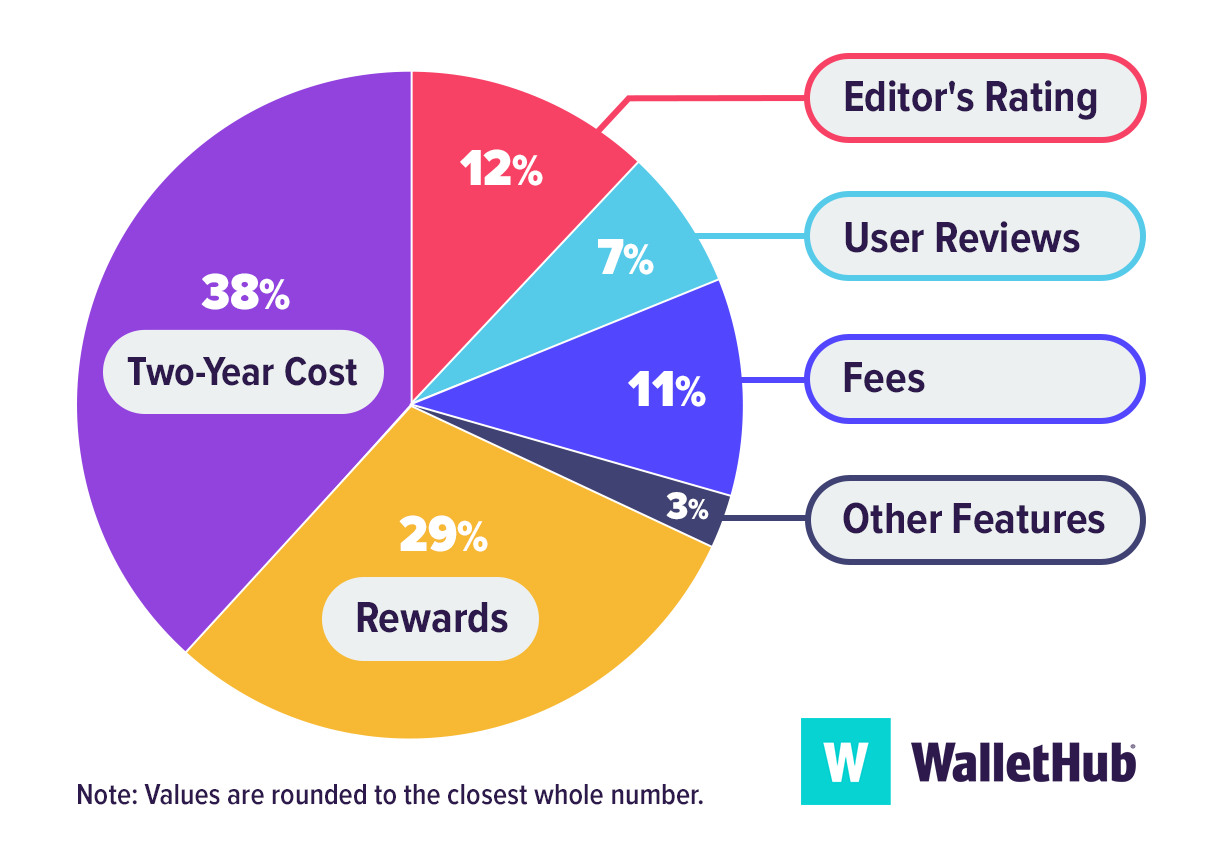

WalletHub’s Key Rating Components

Two-Year Cost: 38% – We measure long-term value by weighing each card’s annual fee against the savings a typical cardholder can generate from rewards over a two year span. Cards that provide consistent, well-rounded value across different spending categories tend to rank higher.

Rewards: 29% – We review each card’s rewards earning and redemption framework, including base earning rates, bonus categories, redemption values, and more. Special attention is given to how practical the rewards are for everyday purchases like groceries, dining, travel, and online shopping.

Editor’s Rating: 12% – Our editors evaluate the extent to which each card stands out within the Mastercard network and against similar cards on other networks. We focus on usability, overall value, and whether the card fits well as a primary card or as part of a broader strategy.

Fees: 11% – We take a close look at all associated costs, such as annual fees, foreign transaction fees, and any other charges. Cards that keep costs reasonable receive better scores.

User Reviews: 7% – We factor in user feedback to capture insights into everyday usage, including customer support, ease of managing the account, and satisfaction with rewards and benefits.

Other Features: 3% – We consider added perks that come with Mastercard products, such as trip cancellation/interruption insurance, rental car coverage, and travel accident insurance, as well as purchase protection, extended warranty coverage, price protection, identity theft monitoring, and concierge services, all of which enhance the overall cardholder experience.

Some cards are also chosen for features like extended introductory APR offers or accessibility for applicants with fair or limited credit, including students. In these cases, we apply a modified scoring approach to better reflect those specific use cases.

How Two-Year Cost Is CalculatedTwo-year cost is used to calculate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that different users have different goals and are likely to use their credit cards differently, we identified spending profiles that are representative of different users’ financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data for consumers and PEX data for businesses.

Sources

WalletHub actively maintains a database of 1,500+ credit card offers, from which we select the best Mastercard credit cards for different applicants as well as derive market-wide takeaways and trends. The underlying data is compiled from credit card company websites or provided directly by the credit card issuers. We also leverage data from the Bureau of Labor Statistics to develop cardholder profiles, used to estimate cards’ potential savings.