Resolution season is a great time to make financial improvements, and more than 1 in 4 Americans are planning to make finance-related New Year’s resolutions for 2026, according to a new WalletHub survey. For example, 31% of people making a financial resolution want to save more money.

To help you make the most of this opportunity for reflection and self-improvement, we put together a list of the top financial New Year’s resolutions for 2026, plus a playbook for making them a reality.

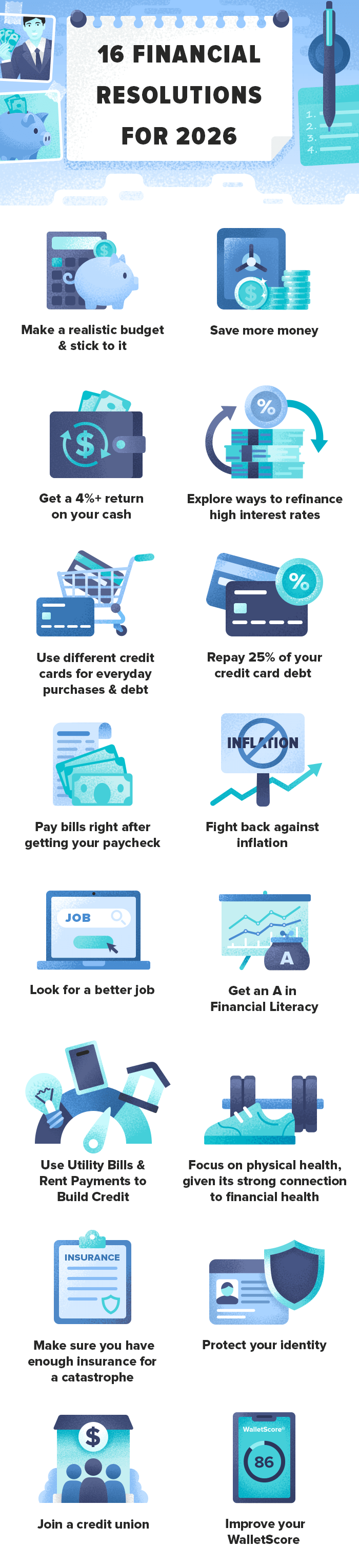

16 Financial Resolutions for 2026

- Make a realistic budget & stick to it

- Save more money

- Get a 4%+ return on your cash

- Explore ways to refinance high interest rates

- Use different credit cards for everyday purchases & debt

- Repay 25% of your credit card debt

- Pay bills right after getting your paycheck

- Fight back against inflation

- Look for a better job

- Get an A in financial literacy

- Use utility bills & rent payments to build credit

- Focus on physical health, given its strong connection to financial health

- Make sure you have enough insurance for a catastrophe

- Protect your identity

- Join a credit union

- Improve your WalletScore

Below, you can learn more about each of WalletHub’s financial resolutions for 2026, including why they’re good for your wallet and how to accomplish them. You can also get more insights about making and keeping New Year’s resolutions from our Q&A with a panel of experts.

Top Financial Resolutions for 2026 & How to Keep Them

-

Make a Realistic Budget & Stick to It

The fact that we’re on pace to end 2025 with over $1.3 trillion in credit card debt is a clear sign that we need to do a better job budgeting. The best way to start budgeting is to sync your credit cards and checking account using a budgeting app like WalletHub. Once you do that, you’ll be able to quickly see where your money goes and identify types of expenses you can cut down on.

Moving forward, make sure to check on your budget at least once a week. You can use the insights from your budgeting app to self-correct and ensure that you are staying on course toward your major financial goals.

-

Save More Money

Millions of Americans do not have a rainy-day fund, according to the Federal Reserve of Minneapolis. Like someone without insurance, people who lack an emergency fund are tempting fate, putting themselves at risk of financial catastrophe in the event of unexpected unemployment or major medical expenses. A lot of people found that out the hard way over the past few years.

So, building up some reserves should be one of the first orders of business for any financial makeover. We recommend ultimately building a fund with about 12 to 18 months’ take-home income. But it’s important to understand that won’t happen overnight. In other words, you don’t need to put the rest of your financial life on hold until your emergency fund is complete. Rather, chip away at it over time by automating monthly transfers from your checking account to your savings account.

Start with a goal to set aside two months’ pay so you’re better prepared for a significant downturn in the economy. After all, more than 2 in 5 Americans think that their household finances are not recession-proof, according to a WalletHub survey. Once you have that safety net, you can add to it at your own pace.

-

Get a 4%+ Return on Your Cash

In recent years, the APYs on bank accounts weren’t high enough to really bother comparing. Now, after numerous rounds of Federal Reserve rate hikes (and only a couple cuts), you can save a lot of money by strategically selecting your bank account. Now, the average online savings account has an APY around 3.27%, and you can get a 4%+ annual return from the best deposit accounts.

If you’d like a recommendation, check out WalletHub’s picks for the best high-yield savings accounts and the best CD rates.

-

Explore Ways to Refinance High Interest Rates

Refinancing opportunities are most abundant when rates are falling, and that’s starting to happen. You are especially likely to find opportunities to save if your credit score and income have gone up since you got your credit card or loan.

For example, the best balance transfer credit cards can help you consolidate debt and pay it off with no interest for as long as 24 months. The best personal loans for debt consolidation give you even longer to pay off consolidated debt, but the APR won’t be quite as low.

Both the best cards and the best loans require at least good credit for approval. You can check your credit score for free right here on WalletHub.

-

Use Different Credit Cards for Everyday Purchases & Debt

The Island Approach involves using different accounts to serve different financial needs, as if they are a chain of islands. The most basic example is using a rewards credit card for everyday purchases and a 0% APR card for balances that you’ll carry from month to month.

Doing so enables you to get the best possible terms on each card, rather than settling for average terms on a single card. It will also help you reduce the cost of your debt, considering everyday purchases won’t be inflating your average daily balance. And if you ever incur interest on your everyday card, you’ll know you spent too much that month.

-

Repay 25% of Your Credit Card Debt

Americans owe way too much credit card debt: more than $11,000 per household. That debt is extremely expensive, too. Something eventually has to give. And you’d much rather that be your outstanding balance, paid down on your own terms, than your ability to afford monthly minimum payments and, in turn, your credit score. So it’s time to get serious about getting out of credit card debt.

Some of the other steps mentioned here – including budgeting, automation and the Island Approach – will help in terms of reducing your future reliance on debt. But the problem of what to do about existing balances still remains. The answer for people with at least “good” credit is the combination of a 0% balance transfer credit card and a credit card calculator, which has the potential to help you save hundreds of dollars while getting out of debt months sooner than you would otherwise.

But it’s probably best to start small. So we recommend making a plan to pay off 25% of what you owe over the course of 2026. That would amount to about $2,755 for the average household, requiring monthly payments of $230 with a card offering 0% on balance transfers for at least 12 months. You can use a credit card payoff calculator to crunch the numbers in your situation, and if you can afford higher payments, by all means make them. The sooner you can reach debt freedom, the better off your wallet will be.

-

Pay Bills Right After Receiving Your Paycheck

Taking care of monthly obligations before letting yourself indulge in any luxury expenses is a helpful budgeting strategy. It gives you a better sense of what you can truly afford and what you can’t. It also helps you avoid ever having a late payment reported to the major credit bureaus, which is one of the easiest ways to damage your credit score. Furthermore, paying your bill early improves your credit utilization, and thus your credit score, by reducing the balance listed on your monthly statement.

We recommend setting up two automatic monthly payments from a deposit account: one for right after payday and another for a couple days before your monthly due date. The second payment will help you avoid interest on any purchases made between your first payment and the end of your billing period. If you don’t know when your billing cycle begins and ends, simply check your monthly statement. You can also request to change it to whatever day of the month is best for you.

To learn more about keeping your payment train on schedule, check out our 8 Tips For Never Missing A Due Date.

-

Fight Back Against Inflation

More than 9 in 10 people think inflation is still an issue, but there are ways you can level the playing field a bit. For example, you could save 5% at your favorite retailers by getting their store credit cards. Most store credit cards require just fair credit for approval and have $0 annual fees, and the best cards give up to 5% back on every purchase. You can start by applying for the card affiliated with the retailer you spend the most money at, then wait at least a few months before applying again.

There are plenty of other ways to stretch your money further in the face of inflation, too, including shopping around for everything you buy, taking advantage of deals and coupons, turning the thermostat down, buying in bulk and cutting back until prices come down. Adopting these strategies basically enables you to adjust your own prices for inflation.

-

Look for a Better Job

Sometimes, we get so caught up in spending less and saving more that we forget to address the other side of the equation: how much we earn. But the benefits of finding a higher-paying job could actually end up outweighing everything else put together.

Even if you don’t switch jobs altogether, you could find opportunities to supplement your income during your free time. Side gigs seem to be everywhere these days.

-

Get an A in Financial Literacy

Financial literacy levels in this country are far too low, and they’re headed in the wrong direction. For example, roughly 35% of Americans now grade their financial know-how at a “C” or below, according to a recent survey conducted by the National Foundation for Credit Counseling.

So start 2026 by taking our WalletLiteracy Quiz and getting a baseline score. Then, throughout the year, study the areas where you struggled and periodically re-test yourself to gauge your progress. Your goal should be to get at least an A- by the time 2027 rolls around.

-

Use Utility Bills & Rent Payments to Build Credit

Using a credit card responsibly is still the easiest way to build credit, but if you want to take things to the next level, consider using a service to report your rent, phone, gas, water, and electric payments to the credit bureaus. For example, WalletHub can report these payments to TransUnion once you sync your checking account. This will increase the volume of positive information added to your report each month.

-

Focus on Physical Health, Given its Strong Connection to Financial Health

There is a clear connection between physical, emotional and financial health. For starters, the average person spends around $15,000 on health care each year. The economy is one of our biggest sources of stress, according to the American Psychological Association. And people who get regular exercise tend to have better credit scores.

This underscores the importance of getting your financial house in order as well as exercising regularly and engaging in other healthy practices aimed at reducing health care costs. It won’t be easy, but this is one resolution that will certainly pay dividends in multiple areas of your life.

“If you begin to make small healthy changes to your diet, increase exercise in small increments, and practice yoga and meditation, you will feel better,” says Deborah Bauer, a distinguished senior instructor of finance at the University of Oregon. “Feeling better will lead to wiser financial decisions that focus on the long term.”

-

Make Sure You Have Enough Insurance for a Catastrophe

Recent years have clearly illustrated the unpredictability of life and the importance of being prepared for the unexpected. If others depend on you, it's essential to secure their well-being even in your absence or if you're unable to work.

In particular, it’s important to take steps such as purchasing life insurance and disability insurance, in addition to making sure you have enough health insurance coverage. Hopefully, your family won’t need to file any claims for a very long time, but it’s better to be prepared.

-

Protect Your Identity

More than 1 million identity theft complaints are submitted to the Federal Trade Commission each year, and having your identity stolen can be extremely frustrating, time consuming and expensive. Some of the fraud that identity thieves commonly perpetrate will get flagged by free credit monitoring services, including unauthorized credit card and loan applications. But things like fraudulent bank account changes and payday loan applications would not.

To better protect yourself, consider upgrading to an identity protection service. For example, WalletHub Premium provides bank account and alternative loan monitoring, plus dark web monitoring, identity theft insurance and other helpful features.

-

Join a credit union

Credit unions often provide lower fees and better interest rates on loans and savings accounts compared to traditional banks, making them a valuable alternative. For example, credit unions offer 61X higher interest rates on checking accounts than regional banks.

You can easily find a credit union you’re eligible for using WalletHub’s credit union search tool.

-

Improve Your WalletScore

Your WalletScore is like your credit score, but it grades your finances overall. In addition to your credit history, your WalletScore evaluates areas such as your spending habits, emergency preparedness and retirement planning to give you a holistic understanding of your financial strengths and weaknesses.

You can check your WalletScore for free on WalletHub and get your personalized improvement plan. All you have to do is follow the recommendations, and your finances will be in better shape.

- To what extent do you think inflation will affect New Year's resolutions this year?

- What are the Do’s and Don'ts of New Year's resolution-making?

- To what extent does a solid support system make it easier to stick to resolutions? Is it a good idea to have a resolution buddy?

- Does rewarding positive behavior make it easier to accomplish a long-term goal? Are certain types of incentives better than others?

- What is the ideal number of resolutions?

- Do you have any tips for people with financial resolutions?

Ask the Experts: Making & Keeping New Year’s Resolutions

We turned to a panel of experts in the fields of personal finance, business, management and psychology for additional insight into the best New Year’s Resolutions for achieving financial improvement and strategies for sticking to them. You can check out our experts’ bios as well as the questions we asked them and their responses below.

Ask the Experts

Associate Professor in Sociology and Psychology - Temple University College of Liberal Arts

Read More

Ph.D. – Director, Strategic Research, School for Professional Studies, Saint Louis University

Read More

Associate Professor, Marketing - Northeastern University’s D’Amore-McKim School of Business

Read More

Ph.D., LMFT – Associate Professor and Internship Director, Couple and Family Therapy Program, Kirk Kerkorian School of Medicine - University of Nevada, Las Vegas

Read More

Ph.D. – Professor of Psychology, Roosevelt University; Financial and Clinical Psychologist

Read More

Associate Professor of Psychology, Faculty Director of Research, College of Arts and Sciences - New York University

Read More

WalletHub experts are widely quoted. Contact our media team to schedule an interview.