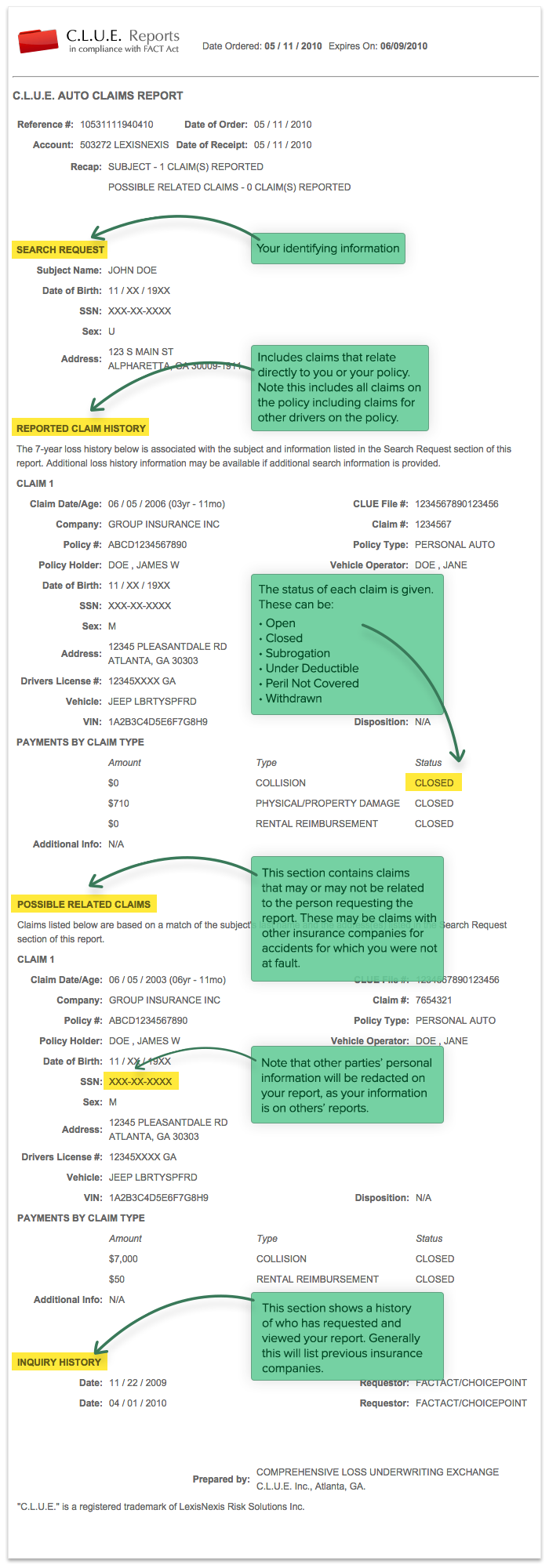

What Is a Clue Report?

A CLUE report is a summary of a person’s auto or home insurance claim history that all major insurance companies consult when they take on a new customer. The CLUE database, which is run by LexisNexis, lets insurers see any claims that a new customer has filed within the last seven years. Verisk offers a similar report, known as A-PLUS, but it’s less commonly used than CLUE.

Every claim that you file will end up on your CLUE report, even if you weren’t issued a ticket or found at-fault for the incident. Once your insurer sees your CLUE report, they may adjust your rates if you’ve neglected to inform them of all claims in your history.

What’s Included in a CLUE Report?

- Your name

- Address

- Date of birth

- SSN

- Previous claims that insurers have paid

- Previous claims that insurers have denied

- Serious inquiries you have made to your agent or adjuster

Do All Insurance Companies Report to CLUE?

More than 99% of auto insurance companies and 96% of home insurance companies contribute to CLUE, according to LexisNexis. Only insurance companies that report information to CLUE can also withdraw information from the LexisNexis database.

What Companies Put on Your CLUE Report

- Claim and the payout amount

- A file if there may be possible claim

- A record when claim is denied

Learn more about whether all insurance companies report to CLUE report.

How Much Does a CLUE Report Cost?

A CLUE report costs $0 for your personal report from LexisNexis. You are entitled to one free copy of their LexisNexis CLUE report each year, while additional reports ordinarily cost $19.95 each. LexisNexis customer service representatives say there is no charge for customers to access additional copies of their own reports, though.

Learn more about how much a CLUE report costs.

How to Get Your CLUE Report for Free

To view your CLUE report, you must request your entire LexisNexis personal report. You can request a copy of your report from LexisNexis Risk Solutions online or by phone:

- Online: LexisNexis Personal Reports

- Phone: (866) 312-8076

The Fair Credit Reporting Act entitles you to a copy of your report from any consumer reporting agency, including LexisNexis’s CLUE, for free once per year. Similarly, a copy of your A-PLUS report from Verisk is available online or by phone (800-627-3487).

Learn more about how to get your CLUE Report for free.

How to Dispute CLUE Report Errors

In light of the CLUE report’s direct impact on your wallet, understanding the contents of your file and checking it for errors is extremely important. The good news is – much like with your credit report – you can request, review, and dispute items in your CLUE report.

Contact Your Insurer: If your current insurer has made an error in what they’ve reported to LexisNexis, you should contact them immediately and notify them of the error.

Contact LexisNexis: They will investigate the errors and the nature of the dispute and remove any information that is found to be incorrect.

You can contact the LexisNexis consumer care center by:

- Phone: 888-497-0011

- Email: [email protected]

- Mail: LexisNexis Risk Solutions Consumer Center / P.O. Box 105108 / Atlanta, GA 30348-5108

Add a Personal Statement: You can add personal statements to your report to clarify claims or details.

Learn more about how to dispute your CLUE report.

Sample CLUE Report

CLUE Report: More Things To Know

- Claims stay on your CLUE report for seven years. Knowing when claims will age out of your report can help you know when to expect a rate drop from your current insurer or when to shop for a new one.

- You are legally entitled to know why an insurer denies you coverage, even if it was because of negative information from CLUE or other reports such as your credit history or driving record.

- Know your FCRA rights regarding consumer reporting. You are entitled to free copies of your CLUE report, an annual free copy of your credit report, and copies of your driving record from your state’s DMV.

- State governments regulate insurance and privacy rights. If you have concerns about a claims history report you cannot resolve, contact your state insurance commissioner.

Video: Understand CLUE Report

Ask the Experts

To gain more insight about CLUE report, WalletHub posed the following questions to a panel of experts. Click on the experts below to view their bios and answers.

1. Why is it important to check your CLUE report?

2. How often should you check your CLUE report?

3. What is the best way for drivers to clean up their CLUE report?

Ask the Experts

Ph.D., Assistant Professor of Supply Chain Management, Broad College of Business, Michigan State University

Read More

Professor of Practice & Adjunct Professor of Law, LEED AP, GGP, Brooklyn Law School

Read More

Assistant Professor of Law, School of Law, University of North Dakota

Read More

Ph.D., CFP®, Professor, Department of Financial Planning, Housing and Consumer Economics, College of Family and Consumer Sciences, University of Georgia

Read More

Associate Professor of Instruction in Law/Forensic Accounting, Lynn Pippenger School of Accountancy/Cyber Florida, Muma College of Business, University of South Florida

Read More

Professor Emeritus, School of Business & Technology, Southwestern College

Read More

WalletHub experts are widely quoted. Contact our media team to schedule an interview.