Credit card fraud is when someone else uses your credit card information to make unauthorized purchases, or when they impersonate you in order to open a credit card account in your name. This is a big problem, as reported cases of credit card fraud cost the U.S. more than $200 million per year, according to the Federal Trade Commission. Some estimates also put the total impact in the billions.

The good news is that credit card fraud doesn’t have to cost you any money. All major credit cards have a $0 liability guarantee for fraudulent purchases, which means you won’t have to pay for unauthorized transactions that you or your credit card company catch. You can also sign up for credit monitoring and identity theft insurance through WalletHub and other companies, for added visibility and protection.

Legal Definition of Credit Card Fraud

The federal laws against fraudulent use of credit cards are 18 U.S. Code § 1029 and 15 U.S. Code § 1644. To put it simply, these laws say that you can’t use, own or produce credit cards that are counterfeit or not authorized for your use. You also can’t transport a credit card across state lines or make purchases affecting inter-state or foreign commerce if the card isn’t yours and you don’t have permission to use it.

18 U.S. Code § 1029

15 U.S. Code § 1644

The penalties for breaking the federal laws against credit card fraud include fines of up to $10,000 - $100,000+ and up to 10 - 20 years in prison.

In addition, states have their own laws against credit card fraud. For example, you can get six months to 10 years behind bars in Texas, up to three years in prison in California, and up to seven years of incarceration in New York. In Florida, you can even get sentenced to as many as 30 years in prison if you engage in very high-value credit card fraud.

How Credit Card Fraud Happens

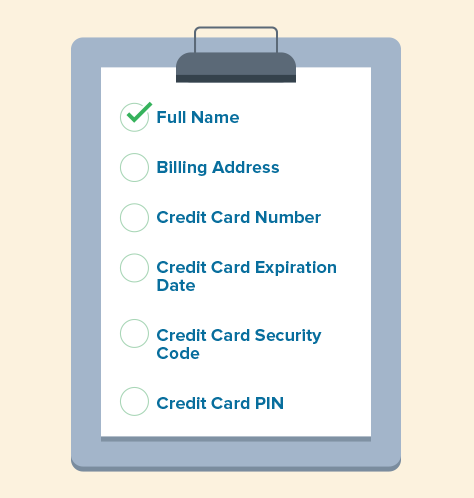

Credit card fraud isn’t complicated – and that’s a big part of why it’s so terrifying to consumers. Scammers simply need to steal a few key pieces of personal information, and voilà! They can either access your funds directly or sell your account information via black market websites.

Here is a list of the most common data points that fraudsters typically target:

Think about how much of the above information is shared every time you make a purchase. While merchants are prohibited from storing your security code and several other pieces of information – such as your PIN and magnetic stripe data – scammers don’t need to abide by such rules.

Here are the methods credit card fraudsters will use to get their hands on your personal info:

Skimming

Skimming is when fraudsters insert a small device into a point of sale machine or ATM, allowing them to record account information from the magnetic stripe whenever plastic is swiped. This information can be used to make a duplicate card.

Computer Hacking

Fraudsters can infiltrate your computer by installing viral spyware on it. This potentially gives them access to the keystrokes you type into your computer, including credit card details as well as account passwords and usernames.

Phishing

While most people think of scammers as computer nerds sitting in a dark room halfway around the world, they can actually be smooth talkers. Whether it’s online or over the phone, they’re adept at contacting individuals under seemingly legitimate pretenses to get them to hand over confidential information. They’ll often have a couple pieces of information about you already, adding to their aura of authenticity.

Mail & Dumpster Diving

You can learn a lot about someone simply by sifting through their trash and mail. Fraudsters aren’t afraid to get their hands dirty – they’ll look for documents such as bank statements, credit card and utility bills, receipts and pre-screened credit card offers in particular.

Stealing

Some thieves also take the old-fashioned route of robbery, simply pickpocketing people for plastic.

- the company’s check-out system. An estimated 56 million card numbers were stolen.

- The Shape-Shifting Thief – Adekunle Adetiloye, who was living on welfare but somehow maintained a lavish lifestyle, was sentenced to jail for about 18 years due to nearly 600 fraudulent credit card accounts opened under multiple peoples’ identities. The elaborate scheme enabled him to steal roughly $1.5 million from over 20 major banks.

What Type of Fraud Is the Most Common?

Fraud can happen in a lot of different ways and affect various types of financial accounts. Fortunately, we have some insight into the details, thanks to the Federal Trade Commission’s Consumer Sentinel Network. Below, you can see the latest annual stats on how fraud and identity theft affect credit cards and more.

Fraud Reports by Payment Method

| Payment Method | Number of Reports | Total Loss

(millions) |

| Credit Cards | 114,348 | $246 |

| Debit Card | 83,370 | $220 |

| Payment App or Service | 65,305 | $210 |

| Bank Transfer or Payment | 51,221 | $1,860 |

| Cryptocurrency | 47,537 | $1,409 |

| Wire Transfer | 42,729 | $344 |

| Gift Card or Reload Card | 41,632 | $217 |

| Cash | 13,656 | $271 |

| Check | 8,603 | $209 |

| Money Order | 3,087 | $45 |

Source: Consumer Sentinel Network Data Book 2023, Federal Trade Commission

Most Common Types of Identity Theft

| Rank | Theft Type | Number of Reports |

| 1 | Credit Card | 416,582 |

| 2 | Other Identity Theft | 260,734 |

| 3 | Loan or Lease | 149,771 |

| 4 | Bank Account | 136,778 |

| 5 | Government Documents or Benefits | 96,951 |

| 6 | Employment or Tax-Related | 89,465 |

| 7 | Phone or Utilities | 79,722 |

Source: Consumer Sentinel Network Data Book 2023, Federal Trade Commission

Credit Card Identity Theft Reports by Account Type

| Type of Account | Number of Reports | Year-Over-Year Change |

| New | 381,122 | -7% |

| Existing | 44,855 | 14% |

Source: Consumer Sentinel Network Data Book 2023, Federal Trade Commission

How to Protect Yourself From Credit Card Fraud

Credit card fraudsters may be upping their game, but that doesn’t mean consumers should stand pat. In fact, there are numerous measures individuals can take to proactively minimize their odds of victimization. And since these strategies don’t require much effort to implement and are fairly commonsensical, you should try to cover as many of these bases as possible.

Cancel Your Card If You Lose It

If you lose your credit card, contact your issuer immediately (unless you’re positive that you’ve lost it somewhere at home or in a private space). You see, even if you’re certain that you left it at a particular bar or restaurant and can arrange to pick it up, someone with malicious intent may have already jotted down your credit card information. So, always follow the “better safe than sorry” motto and cancel the card.

Check Your Credit Card Statement

Make it a standard practice to cross-reference credit card receipts with monthly credit card bills in order to spot unauthorized charges. Not only is this useful for budgeting purposes, but it’s one of the easiest and quickest ways to detect credit card fraud.

Augment Your Fraud Protection

While all card networks provide $0 fraud liability guarantees, you may want to keep a closer eye on your finances with a credit monitoring service and get identity theft insurance just in case. Several credit card companies also feature text alerts that are sent every time the card is swiped, thereby notifying the cardholder if the account is ever hijacked. Check with your issuer and network to see what specific fraud protection services they can offer you.

Protect Your Identity

Generally safeguarding your identity will help prevent credit card fraud by minimizing the chances that personal information becomes available to the wrong people. Check out our Identity Theft guide to learn about preventive measures like checking your credit reports and shredding your documents.

Leave No Room For Doubt

Never leave the final amount of a transaction open for interpretation. That means, for example, making sure to always fill in the “Tip” field on a bill, even if you’re only going to write “$0.00.”

Avoid Public Computers

Never enter credit card information on public computers. A lot of different people use them, leaving them unsecured and especially susceptible to spyware.

Secure Your Wireless Network

Make sure your home and office internet connections require passwords to connect. Public wireless networks are much more vulnerable to “middle-man” attacks, which are when a third party hacker intercepts the information sent between a user and the internet server they’re connected to.

The good news is that credit card users are protected. All of the major card networks extend $0 fraud liability guarantees to cardholders. As long as you report suspected fraud within a reasonable timeframe (your issuer is watching for signs of fraud and may notify you of any issues as well), you will not be held responsible for any unauthorized charges.

Each card network’s fraud liability policy is a bit different, however – especially as they relate to debit cards. So make sure to check out WalletHub’s latest Credit & Debit Card Fraud Liability Study for more information on how to report your case.

WalletHub's personal finance experts are frequently cited by leading media outlets. Contact our media team to arrange an interview.