Direct deposit is an automatic electronic transfer that allows regularly scheduled payments, such as salary, pension, government benefit, tax refund and investment payments, to be made straight to your bank account. It is made possible by Automated Clearing House (ACH), an electronic network that lets banks bundle multiple transactions together and process them in batches.

Direct deposit offers a convenient, secure and reliable alternative to the traditional paper check, but should not to be confused with direct payment using ACH credit or debit, which is commonly used for shopping or paying bills online.

How Direct Deposit Works

On the face of it, direct deposit is straightforward. All you have to do is set up a direct deposit once with the payer, and then the recurring payment appears in your account every time the payer initiates one. Everything else happens behind the scenes.

Let’s take your employer’s payroll as an example. The payer, in this case your employer, instructs their bank to transfer your payroll earnings into your account. This order is then bundled up with all the other ACH transactions for that day and scheduled to be transferred. On payday, your bank credits the funds to your account, and your employer’s bank debits their account for the same amount.

If you don’t have a bank account, another option is to use a prepaid debit card, also called a payroll card when used for payroll earnings. The direct deposit works in exactly the same way, only instead of being transferred into a bank account, the money is paid directly onto your card. You can then use your prepaid debit card to withdraw money from an ATM or pay at a point of sale just like you would with a traditional debit card attached to a checking account.

How To Set Up Direct Deposit

Setting up a direct deposit is easy.

Let’s continue with the example from earlier. To receive your paycheck by direct deposit, you’ll have to fill out and submit a direct deposit authorization form to your employer. This form will request four pieces of information that are needed to properly route your payments:

- The name of your bank or credit union

- Your account type – checking or savings

- Your account number

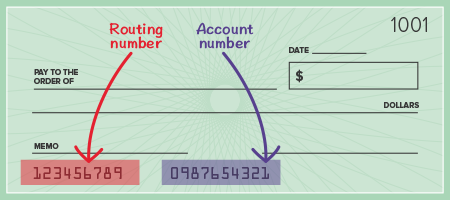

- Your bank’s ABA routing number

You may also be asked to provide a voided check – this is done to verify your account and routing numbers (which can be found at the bottom of a check) and to avoid any clerical errors. This can be an obstacle, as some people don’t use paper checks anymore. In this case, you may be required to get a document from your bank that confirms your account number and the bank’s routing number.

Some banks now make it possible for you to access a boilerplate direct deposit authorization form, which you can fill out online, through your personal banking profile. Once you’ve completed the form, all you have to do is print it and mail it to the payer so that they can then initiate the transfer.

While some small employers may not offer direct deposit of payroll, it is increasingly common for some businesses to require all employees to receive their paycheck by direct deposit. In these cases, the employer generally will offer an affordable prepaid debit card to any employees who lack their own bank accounts.

Splitting Direct Deposits Among Multiple Accounts

Some payers will allow you to split your direct deposit among multiple accounts. There are three ways you can designate how funds will be deposited.

| Deposit Type: | Example: |

|---|---|

| Amount | A fixed amount, for example $50.00. |

| Percentage | A percentage of the total payment, for example 25%. |

| Balance/Remainder | The remainder of your payment, less any fixed amounts or percentages that have been directed to another account. |

Splitting direct deposits can be particularly useful if you’re trying to add to your savings, since you can designate part of your paycheck to go straight into your savings account, while assigning the remainder to your checking account for general use. Sending funds straight to your savings account can help reduce the temptation to overspend.

Benefits of Direct Deposit

Direct deposit has a number of advantages. These include:

- Convenience: Once you’ve set up a direct deposit, the transfer takes place automatically, with no further action required on your part. This means that whether you’re on vacation in the Bahamas or stuck in bed with a cold, you can expect your money to come through directly to your account without ever having to set foot in a bank.

- Security: According to Javelin Strategy & Research, an independent strategy and research consultancy, almost 85% of identity theft starts with offline transactions—in other words, with a lost or stolen check or billing statement. Direct deposit eliminates the possibility of losing or having a check stolen and therefore reduces the risk of identity theft and fraud.

- Reliability: Direct deposit takes place electronically, thereby avoiding third party delays from couriers and eliminating the risk of having checks lost in the mail.

- Speed: Funds transferred to your account by direct deposit are available immediately. This is not always the case with paper checks as banks may put your funds on hold to account for the time it takes for checks to clear. In addition, because direct deposits are simpler to process than paper checks, they can speed up payments like tax refunds that otherwise might take days or weeks to generate.

- Flexibility: Direct deposits are easy to set up and easy to change or cancel. All you have to do is submit a new direct deposit authorization form and/or written confirmation of your request to the payer.

- Access To Free Checking: It is common for banks to waive any monthly account maintenance fees for customers who receive regular direct deposits into a checking account. Without direct deposit, you may be required to maintain a minimum balance to avoid monthly fees.

- Environmentally Friendly: Going paperless doesn’t mean just saving the trees used to make the checks, you’re also saving fuel and cutting the emission of harmful greenhouse gases into the environment. PayItGreen, a collaborative initiative led by NACHA, the Electronic Payments Association, claims that the use of paper checks consumes over 674 million gallons of fuel and emits more than 3.6 million tons of greenhouse gases every year.

If There Are Problems

Although problems with direct deposit are rare, they can occur, and it’s important to know what to do if something goes wrong.

If you’ve just set up your direct deposit, it can take one or two payment cycles before you receive your first payment electronically. This is because many payers test your account with a zero dollar deposit to make sure that all the information is correct before transferring funds.

Aside from this potential delay, common problems with direct deposit include:

- The transfer didn’t go through: Don’t panic. Most errors that occur with direct deposits are easily explained or remedied. Changes in the payroll process, inaccurate information, and irregular paydays due to holidays can all result in your money not turning up when you’re expecting it. You simply need to contact the payer and your bank so that they can remedy the problem.

- The transfer came through but in the wrong amount: It’s important that you remember to check your pay stub against your bank statement to make sure you’ve been paid the correct amount. If not, you should contact your bank and the payer.

- The transfer was made twice: Although a payer cannot access or withdraw money from your account, they do have a five day window in which they can recall payments made in error without notifying you. Unfortunately that doesn’t mean the money becomes yours once those five days are up. It still belongs to the payer, but they will now have to deal directly with you, the account holder, to rectify the error.

WalletHub experts are widely quoted. Contact our media team to schedule an interview.