Methodology

To select the best Amazon credit cards, WalletHub’s editors regularly compare all the credit cards co-branded with Amazon.com from our database of 1,500+ credit card offers based on factors such as their approval requirements, rewards-earning rates, APRs and other WalletHub Rating components.

In addition, we consider cards that don’t have Amazon branding but do have a special connection with the company. For example, cardholders may earn bonus rewards on Amazon purchases or have the opportunity to redeem their rewards to pay for Amazon purchases.

Final selections are made based on the estimated two-year cost of each card.

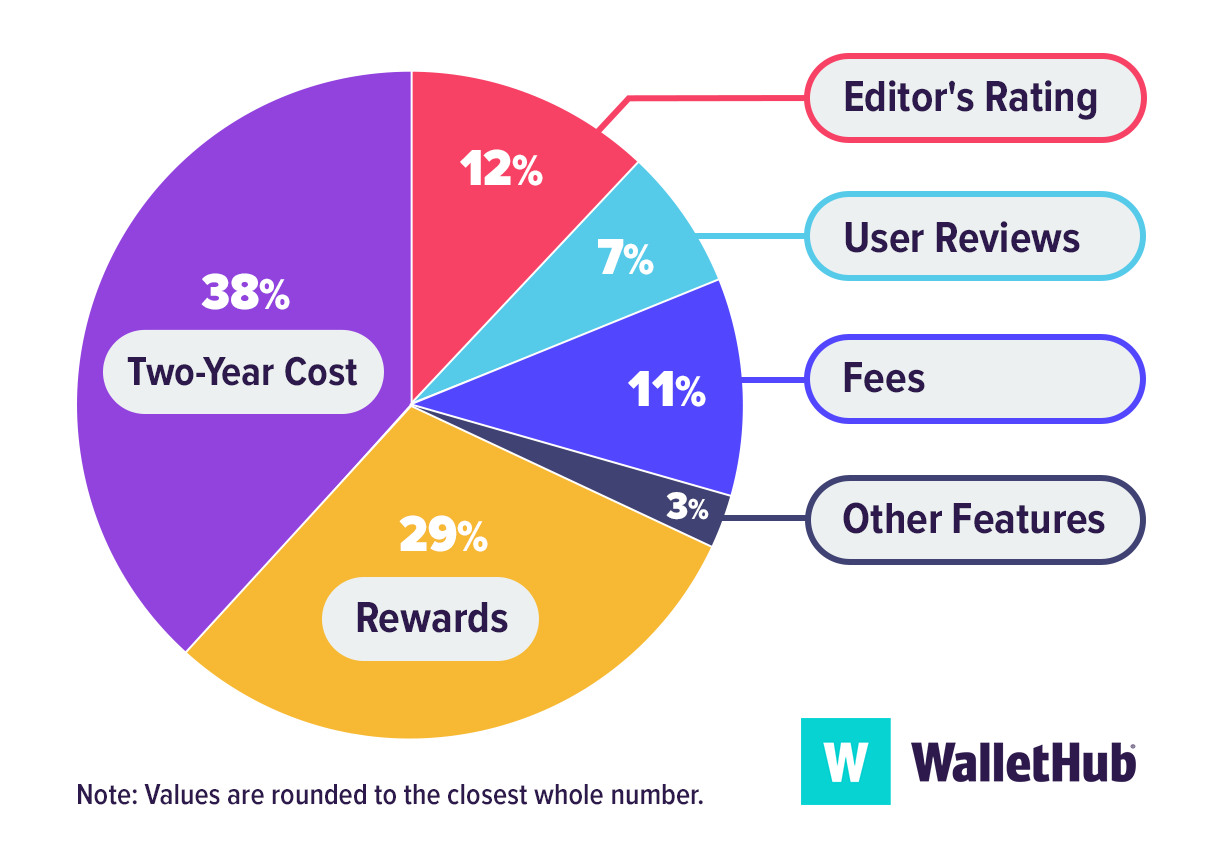

WalletHub's Key Rating Components

Two-Year Cost: 38% – We calculate the average cardholder’s net cost over two years by considering annual fees along with rewards earned from Amazon purchases and everyday spending.

Rewards: 29% – We review how rewards are earned and redeemed, focusing on reward rates for Amazon purchases, redemption flexibility, and the estimated overall value for the average cardholder.

Editor’s Rating: 12% – WalletHub editors evaluate each Amazon credit card based on its rewards structure, usefulness for different types of Amazon shoppers (including Prime members and non-members), fee structure, and overall value compared to similar credit cards.

Fees: 11% – We examine all fees associated with the card, including annual fees, monthly fees, and other potential charges that may impact the overall value.

User Reviews: 7% – We consider feedback from cardholders to assess satisfaction with rewards, billing, customer service, and the overall experience.

Other Features: 3% – We account for additional card features such as special financing offers, exclusive Amazon discounts, extended return periods, and purchase protection.

How Two-Year Cost Is CalculatedTwo-year cost is used to approximate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that people have differing goals and are likely to use their credit cards differently, we identified spending profiles that are representative of varied financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data for consumers and PEX data for businesses.