- Best credit cards for online shopping compared

- Online shopping credit card tips

- Methodology

- Sources

- About the author

- User questions & answers

Best Credit Cards for Online Shopping Compared

| Card Name | Best For | Rewards Rate | Annual Fee |

| Wells Fargo Active Cash® Card | Overall | 2% cash rewards | $0 |

| Blue Cash Preferred® Card from American Express | Big-Spenders | 1 - 6% cash back | $0 intro 1st yr, $95 after |

| Chase Freedom Unlimited® | Low APR & Rewards | 1.5 - 5% cash back | $0 |

| Prime Visa | Shopping on Amazon | 1 - 5% cash rewards | $0 |

| Target Credit Card | Department Store | 5% discount | $0 |

| Petal® 2 Visa® Credit Card | No Credit | 1 - 1.5% cash back | $0 |

Online Shopping Credit Card Tips

Check your credit score before comparing cards

The very best credit cards for online shopping require good or excellent credit for approval, which means a credit score of 700 or higher. There are still great options for people with lower scores, too. But to find a good deal with high approval odds, you need to know your credit score. You can check your latest credit score for free on WalletHub.

Have clear intentions for what you’ll use the card for

Knowing exactly how you’ll use your new credit card will help you focus on comparing the card features that will impact you the most. For example, if you’re going to use the card on one particular retailer’s website or for a certain category of purchases, you can concentrate on the cards that will give the most rewards on those purchases. Or, if you mainly want to take advantage of a card’s initial bonus, you don’t have to pay as much attention to its ongoing features.

Consider retailer-affiliated credit cards

Store credit cards and co-branded credit cards affiliated with major retailers are some of the best credit cards for online shopping because they give great rewards and usually have $0 annual fees. You can find cards affiliated with most of your favorite brands, too, and they often require just fair credit for approval.

Be careful not to overspend

It’s easy to get carried away when shopping online, but spending beyond your means is a costly mistake. Unless your card has a low-interest promotion, you’re likely to rack up expensive interest charges that eat into your rewards.

Methodology for Selecting the Best Credit Cards for Online Shopping

To identify the best credit cards for online shopping, WalletHub’s editors regularly compare more than 1,500 credit card offers based on their initial bonuses, ongoing rewards, APR promotions, annual fees, approval requirements and other WalletHub Rating components. This enables us to determine which cards are best suited to maximize cardholder savings over a span of two years, for different types of online shoppers.

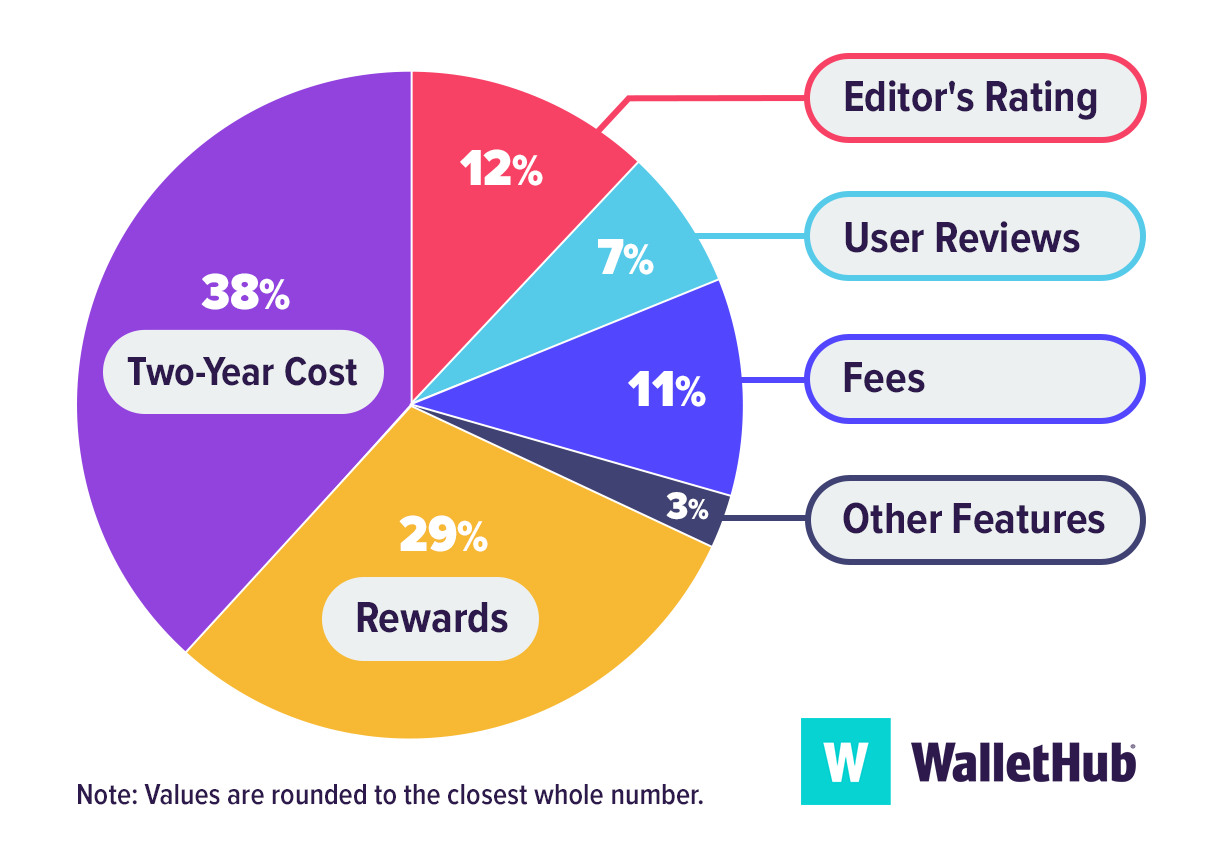

To identify the best credit cards for online shopping, WalletHub’s editors regularly compare more than 1,500 credit card offers based on their initial bonuses, ongoing rewards, APR promotions, annual fees, approval requirements and other WalletHub Rating components. This enables us to determine which cards are best suited to maximize cardholder savings over a span of two years, for different types of online shoppers.WalletHub's Key Rating Components

Two-Year Cost: 38% – We evaluate each card’s overall value over a two-year period by comparing annual fees against the rewards, discounts and statement credits earned through typical online shopping and everyday spending. Cards that provide strong returns on e-commerce purchases while keeping net costs low receive higher scores.

Rewards: 29% – We assess the value cardholders earn via rewards, considering the base rewards rate, earning rates in bonus categories relevant to e-commerce, and redemption rates.

Editor’s Rating: 12% – Our editors examine each card’s overall value for online shoppers, focusing on long-term earning potential and how it compares with other cards designed for frequent online spending.

Fees: 11% – We review all associated costs, including annual fees, foreign transaction fees (important with international online retailers), balance transfer fees, and penalty charges. Cards with minimal fees and transparent terms score higher.

User Reviews: 7% – We consider feedback from cardholders, with special attention to customer service quality, dispute resolution for online purchases, fraud protection experiences, rewards reliability, and overall satisfaction.

Other Features: 3% – We factor in additional benefits that enhance online shopping, such as purchase protection, extended warranties, return protection, introductory APR offers, and card acceptance.

Some cards featured on this page are designed for consumers with bad, limited, or fair credit, while others are co-branded options that provide enhanced rewards for shopping with specific retailers. Because these cards are built to serve different needs, we apply a modified scoring approach to more accurately reflect their unique benefits, limitations, and overall value for their intended audience.

How Two-Year Cost Is CalculatedTwo-year cost is used to approximate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that different credit card users have different goals and are likely to use their cards differently, we identified spending profiles that are representative of people’s varied financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data.

If more of your shopping is done in person than online, you can also check out our best credit cards for shopping overall for a more diverse selection.

Sources

WalletHub actively maintains a database of 1,500+ credit card offers, from which we select the best credit cards for online shopping for different applicants as well as derive market-wide takeaways and trends. The underlying data is compiled from credit card company websites or provided directly by the credit card issuers. We also leverage data from the Bureau of Labor Statistics to develop cardholder profiles, used to estimate cards’ potential savings.