| Credit Card | Best For | Annual Fee | Min. Credit |

| Blue Cash Preferred® Card from American Express | Overall | $0 intro 1st yr, $95 after | Good Credit |

| Wells Fargo Active Cash® Card | Cash Back | $0 | Good Credit |

| U.S. Bank Shopper Cash Rewards™ Visa Signature® Card | Cash Bonus | $0 intro 1st yr, $95 after | Excellent Credit |

| First Federal Community Bank Zero+ Card | Intro APR | $0 | Good Credit |

| Prime Visa | Online Shopping | $0 | Good Credit |

| Target Credit Card | One-Stop Shopping | $0 | Fair Credit |

| Capital One SavorOne Cash Rewards Credit Card (see Rates & Fees) | Fair Credit | $39 | Limited History Credit |

| Petal® 2 Visa® Credit Card | No Credit | $0 | Limited History Credit |

| Capital One Savor Student Cash Rewards Credit Card (see Rates & Fees) | Students | $0 | Limited History Credit |

| Ink Business Cash® Credit Card | Parents with a Small Business | $0 | Good Credit |

Back-to-School Savings Tips

Shopping during sales and paying with the right credit card are two important ways to save on back-to-school shopping. But they aren’t the only ones. Here are some more tips for starting the school year with an “A” in personal finance:

Shopping during sales and paying with the right credit card are two important ways to save on back-to-school shopping. But they aren’t the only ones. Here are some more tips for starting the school year with an “A” in personal finance:

- Stick to a Budget – It’s hard to avoid overspending if you don’t have both a shopping list and a budget. So before heading to the store, make a list of what you need and do a quick search to see how much each item costs. This will help you make an overall back-to-school budget and decide how to allocate the funds. And that will give you a sense of whether you can afford to splurge on certain items as well as make it easier to avoid impulse buys.

- Comparison Shop – It’s easier than ever to shop around for the best deals. So it’s worth doing, at least for big-ticket items. Similarly, don’t rule out shopping online for fear of shipping charges. More and more retailers are offering free shipping options. And you may enjoy the added benefit of shopping tax-free without being limited to a few-day window.

- Avoid Trends – Buying the “latest” goods — from the computers to clothing styles — is a great way to overspend. Saving is the name of the game at back-to-school time, so concentrate on things that were “hot” — last year. Such items will have cheaper starting prices and are more likely to be on sale as well. All you’ll need to do is convince your children that vintage is cool.

- Don’t Go Overboard on Electronics – Kids these days have access to more types of electronics than ever before, and it’s easy for a young person to convince themselves that they need each of these toys. They may even try to convince you that they’ll use the computers, tablets, smart watches, and even video games to learn rather than for games and social media. Your job is to bring some discipline to the back-to-school process. Some popular electronics do have academic applications, but make sure not to acquiesce to every request. Perhaps choose to give your child one of the things they have their eye on, but maybe for their birthday or the holidays, rather than giving them instant gratification.

- Make One Trip – Buying everything you need for the new school year in one fell swoop will help reduce the stress and time involved in the process. Doing so will also help you take full advantage of sales tax holidays as well as the one-time discounts that many store cards offer. Keep in mind that we mean you should make only one trip to a physical store. Shopping online is more accessible and can be used to supplement anything you may forget.

- Buy in Bulk – Looking way ahead can pay extra big dividends. So what school supplies will your child need throughout the whole year? Buying more now will likely get you better prices overall, considering that back-to-school sales don’t last all year.

- Save for College – Why not use back-to-school season as an annual reminder to contribute money to your child’s college fund and evaluate your saving progress? After all, it’s the best gift you could give your child, both educationally and economically speaking. For a complete breakdown of the best ways to save for college, check out our Guide to College Savings Funds.

Methodology for Selecting the Best Back-to-School Credit Cards

To identify the best back-to-school credit cards for parents each year, WalletHub’s editors compare more than 1,500 credit card offers based on their rewards, fees, APRs, initial bonuses, approval requirements and overall suitability for back-to-school season. In particular, we focus on cards with benefits conducive to saving on school supplies, clothing, electronics, and other key purchase categories. The qualifying cards with the lowest two-year cost are ultimately selected.

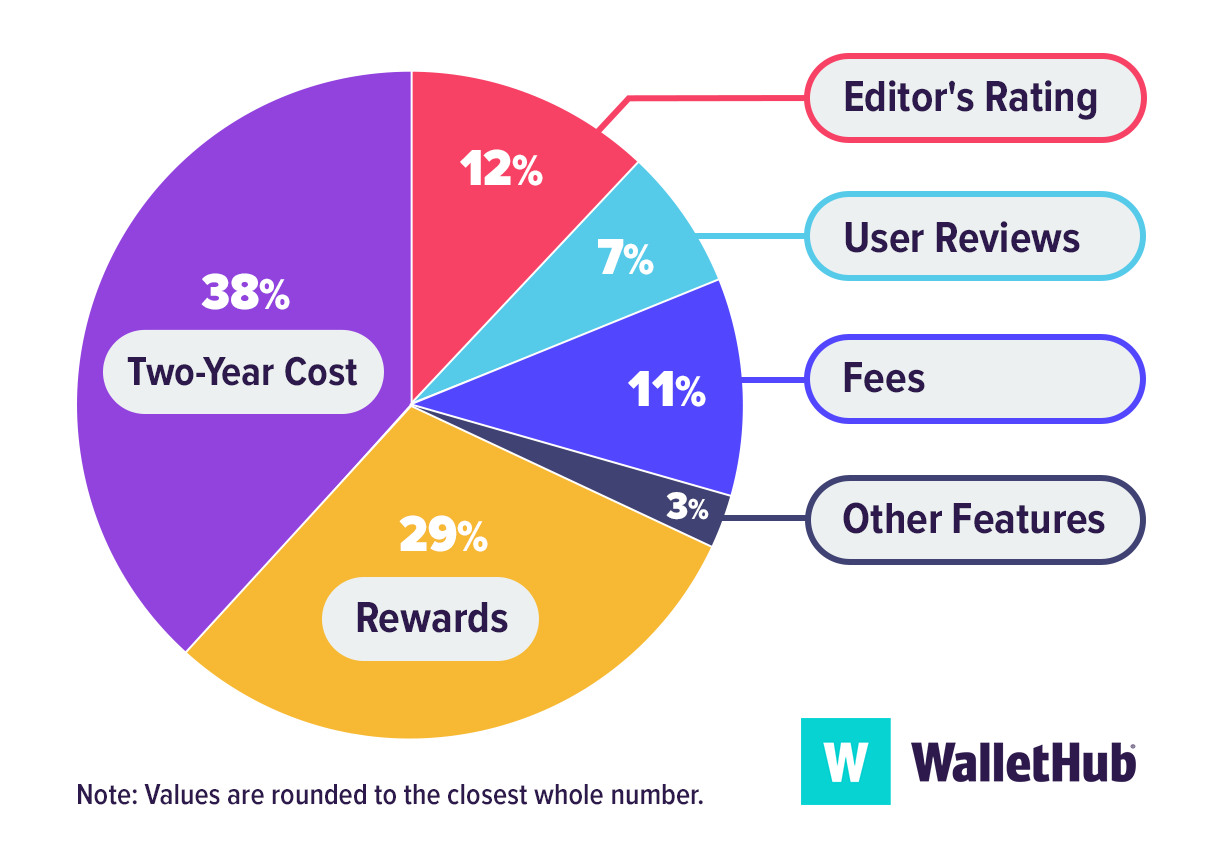

WalletHub’s Key Rating Components

Two-Year Cost: 38% – We estimate the net cost for the average cardholder over a two-year period by factoring in annual fees and the rewards earned from common back-to-school purchases, such as school supplies, clothing and electronics, along with transportation and everyday household spending.

Rewards: 29% – We evaluate how rewards are earned and redeemed, emphasizing bonus categories relevant to back-to-school spending, redemption flexibility, and the overall expected value for parents.

Editor’s Rating: 12% – WalletHub editors assess each credit card based on its rewards structure, affordability, usefulness for families, promotional financing options, and overall value for parents managing back-to-school expenses.

Fees: 11% – We review all applicable costs, including annual fees, foreign transaction fees, monthly fees, and any additional charges that could affect long-term value.

User Reviews: 7% – We incorporate feedback from cardholders to gauge satisfaction with rewards, ease of use, and the overall experience.

Other Features: 3% – We consider added benefits such as introductory APR offers, purchase protection, extended warranties, and special financing options that can help parents manage larger back-to-school purchases.

Some of the cards featured on this page may also be suitable for families who want to help teens or young adults build credit, or for individuals with lower credit scores. These cards use a slightly different scoring methodology.

How Two-Year Cost Is CalculatedTwo-year cost is used to approximate the monetary value of cards for better comparison and is calculated by combining annual and monthly membership fees over two years, adding any one-time fees or other fees (like balance transfer fees), adding any interest costs, and subtracting rewards. Negative amounts indicate savings. When fees or other terms are presented as a range, we use the midpoint for scoring purposes.

Rewards bonuses and credits have been taken into account for two-year cost calculations. However, bonuses applicable to only a very small portion of cardholders are not considered. For example, credits and bonuses awarded for spending or redeeming rewards through a company portal with non-co-branded cards have not been taken into account. Similarly, bonuses and credits related to spending with specific merchants using a non-co-branded card have not been taken into account (for example, if Card A offers credits with DoorDash, this feature would not be factored into calculations because it is hard to assess how many cardholders would use the benefit or exactly how much value they'd get from it).

Cardholder Spending Profiles

Given that different users have different goals and are likely to use their credit cards differently, we identified spending profiles that are representative of different users’ financial priorities and behaviors. For each cardholder type, we have assumed a specific amount of monthly spending by purchase type (e.g., groceries, gas, etc.), as well as an average balance, balance transfer amount, amount spent on large purchases and average monthly payment. Spending assumptions are based on Bureau of Labor Statistics data for consumers and PEX data for businesses.

Small business credit cards often provide excellent rewards, and parents who own a small business could use such a card to save big during back-to-school season.